Privacy Fence Financing Options for Connecticut: Budget & Fund Your Project

A new privacy fence is an excellent addition to any home, but it is also a significant investment. The good news is you do not have to pay for the entire project at once. Many homeowners use financing to make the project affordable, turning a large upfront cost into manageable monthly payments.

Why Financing Your Privacy Fence Is a Smart Move

A quality fence provides privacy, enhances your home's appearance, and creates a safe space for your family. However, the total cost can seem like a major obstacle. That is where privacy fence financing can help. It is not about taking on unnecessary debt; it is about making a valuable home improvement project affordable right now.

Instead of delaying your plans or using all your savings, financing allows you to get the quality fence you want. Homeowners often use financing as a way to upgrade from a basic option to more durable, long-lasting materials like beautiful cedar or low-maintenance vinyl. It is a practical way to invest in your property's value without the immediate financial strain.

A Worthwhile Investment for Connecticut Homeowners

In Connecticut, a professionally installed fence is more than just a property line—it is a solid investment. With strong property values across the state, adding a high-quality fence can increase your home's value by improving both its function and its appearance.

To help you find the right solution, we will explain the most common financing options available. These generally fall into three main categories:

- Unsecured Personal Loans: These are simple loans with fixed interest rates and predictable monthly payments, so you always know what to expect.

- Home Equity Lines of Credit (HELOCs): If you have built-up value (equity) in your home, a HELOC can be a great option, often with lower interest rates.

- Contractor and Third-Party Financing: Many installers, including our team, offer convenient financing options directly, sometimes with special promotional rates.

Understanding these financial tools is the first step. The goal is to install a fence that transforms your yard, without putting your budget under pressure.

Making a smart decision starts with having all the facts and working with a team you can trust. Since 2014, we have served communities across Connecticut and learned that clear communication and transparent planning are essential. You can read about the Connecticut Fence Works story to see our commitment to quality work firsthand. We are here to make the process simple, so a beautiful, durable fence is well within your reach.

Accurately Budgeting Your Connecticut Privacy Fence Project

Before applying for privacy fence financing, you need a solid budget. A realistic budget is the most important part of starting your project without unexpected costs later. It allows you to approach a lender or complete an application with confidence.

So, where do you start? Use a measuring wheel or a long tape measure to walk the exact path where you want the fence installed. Getting this measurement, known as the linear footage, is the first and most critical piece of the puzzle.

Key Factors That Influence Your Fence Cost

Once you have the total length, you can explore the details that determine the final price. It is similar to customizing a car—the base model has one price, but every added feature changes the final cost.

Here are the main variables you will need to consider:

- Fence Material: The material you choose significantly impacts the cost. Classic wood fences, like cedar, have a different cost and maintenance schedule compared to modern, easy-care vinyl. Each has its pros and cons regarding appearance, durability, and upfront price.

- Fence Height: A standard 6-foot privacy fence is the most common choice, but if you need an 8-foot fence for extra privacy or noise reduction, expect the cost to increase. Taller fences not only use more material but often require a more robust installation, which adds to the labor cost.

- Gate Selection: Gates are a project within a project. They are more complex to build and install than a standard fence panel, so a simple walk-through gate will cost less than a wide double gate for a driveway.

- Property-Specific Challenges: Is your yard a flat, perfect rectangle, or does it have hills and slopes? Sloped ground requires more labor and skill to install correctly, which will be reflected in the quote.

Don't Forget Project-Specific Requirements

In addition, your specific needs can influence the budget. For example, if you are fencing a pool area in Connecticut, you must follow strict local safety codes for height, gate latches, and the spacing between pickets. These are legal requirements that can dictate your material and design choices.

Perhaps your main goal is to prevent a large, energetic dog from jumping the fence. In that case, you might want a taller, sturdier build. That peace of mind is worth it, but it is a factor you need to include in your budget.

A professional estimate is not just an approximate figure; it is the concrete number you will provide to lenders. When you approach a bank with a detailed quote from a trusted installer, it shows you are serious, organized, and have done your research.

It is easy to see why some homeowners delay installing a new fence. Studies show that initial costs are a barrier for an estimated 25-40% of potential buyers. That is precisely why financing is such a powerful tool. The demand for privacy and security is driving the global fencing market, which is projected to grow from USD 31.1 billion in 2025 to USD 52.3 billion by 2036. Financing helps homeowners keep up.

Ultimately, the best way to get a real number for your budget is to have a professional visit your property. An expert can measure the area, listen to your needs, identify challenges you might have missed—like rocky soil or complex property lines—and provide a detailed, line-by-line quote. That document is your key to securing the right privacy fence financing and making your project a reality.

So you have a quote for your new privacy fence—great! Now comes the big question: how will you pay for it? Thinking about privacy fence financing can feel overwhelming, but it is really just about finding the right tool for your situation. The best option for you depends on your financial picture, how quickly you want the project done, and your comfort level with different payment plans.

Let's review the most common ways homeowners and businesses fund their fence projects. Once you understand how each one works, including its advantages and disadvantages, you can make a smart choice that fits your budget just as well as your new fence will fit your property.

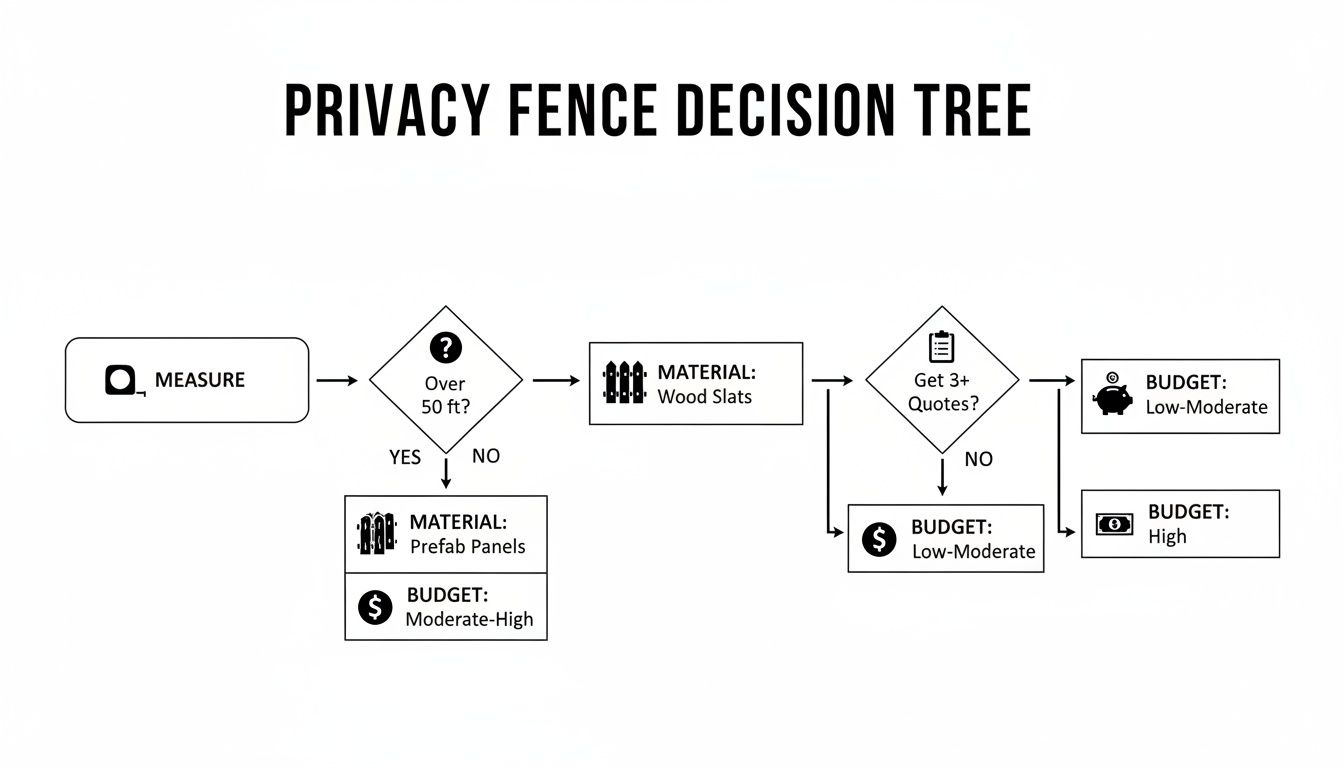

This simple decision tree can help you visualize the first few steps—measuring your yard, choosing a material, and getting a professional quote—which are the foundation for any financing application.

As you can see, having a solid plan and a firm quote is where it all begins. Without those, you cannot effectively compare your financing options.

Comparing Your Privacy Fence Financing Options

This table breaks down the key features of the most common financing methods to help you decide which is the best fit for your budget and timeline.

| Financing Type | Typical Interest Rate | Best For | Key Pro | Key Con |

|---|---|---|---|---|

| Personal Loan | 6% – 36% | Fast funding & predictable payments | Fixed monthly payments make budgeting easy. | Rates are higher, especially without excellent credit. |

| HELOC | Variable; often lower | Larger projects & homeowners with equity | Very flexible; borrow only what you need. | Your home is used as collateral. |

| Contractor Financing | 0% intro, then higher | Convenience & promotional offers | Simple, one-stop process with potential 0% APR deals. | High interest kicks in after the promo period. |

Each path serves a different purpose. A personal loan is quick and straightforward, a HELOC offers flexibility if you have home equity, and contractor financing provides convenience.

Unsecured Personal Loans

A personal loan is one of the most direct ways to pay for a home improvement project. You borrow a lump sum from a bank, credit union, or online lender and pay it back with fixed monthly payments over a set period, usually 2 to 7 years. It is "unsecured," which means you do not have to offer an asset like your house as collateral.

What We Like About Personal Loans:

- Predictable Payments: The interest rate is fixed, so your payment is the same every month. This eliminates surprises and makes budgeting simple.

- Fast Funding: Online lenders can often approve you and provide the funds in just a few business days, which is ideal if you want to start quickly.

- No Home Equity Needed: This is a major benefit for newer homeowners or anyone who prefers not to link a loan to their house.

What to Watch Out For:

- Higher Interest Rates: Since the lender takes on more risk without collateral, the rates are generally higher than for a home equity loan, especially if your credit is not perfect.

- Credit Score is Key: Your credit score heavily influences whether you get approved and the interest rate you will pay.

Real-World Scenario: Imagine a family in Fairfield County needs a pool-compliant fence installed quickly before summer. A personal loan provides the money they need fast, and the fixed monthly payment fits into their household budget without affecting their mortgage.

Home Equity Lines of Credit (HELOCs)

A Home Equity Line of Credit (HELOC) allows you to borrow against the value (equity) you have built in your home. It functions like a credit card with a much better interest rate, where your house secures the loan. You are given a credit limit and can draw funds as needed during a "draw period," paying interest only on the amount you use.

The fencing industry is experiencing massive growth, projected to expand from USD 29.36 billion in 2023 to nearly USD 50 billion by 2033. With safety concerns driving over 60% of installations, financing options like HELOCs are becoming a popular choice. For Connecticut homeowners, using home equity to install a durable vinyl or chain-link fence is a smart investment that can boost property value and security.

What We Like About HELOCs:

- Lower Interest Rates: Because your home serves as collateral, lenders offer very competitive rates—often much lower than personal loans.

- Flexibility: You borrow only what you need, when you need it. This is very helpful if the project scope might change or if you want to fund other home improvements at the same time.

- Potential Tax Deductions: You may be able to deduct the interest paid on a HELOC if the funds are used for home improvements. It is always wise to consult a tax professional about this.

What to Watch Out For:

- Your Home is at Risk: This is the most significant consideration. If you cannot make the payments, the lender can foreclose on your property.

- Variable Interest Rates: Most HELOCs have variable rates, meaning your payment could increase if market rates rise.

- Longer Application Process: Getting a HELOC takes longer than a personal loan. It usually requires a home appraisal and can take several weeks to finalize.

Contractor and Third-Party Financing

To simplify the process for customers, many fence contractors—including us at Connecticut Fence Works—partner with lenders to offer financing directly. This option combines the project and the loan into one convenient package.

What We Like About Contractor Financing:

- Ultimate Convenience: You handle everything with your installer. They guide you through a simple application process that is often decided in minutes.

- Promotional Offers: These programs are known for special deals, such as 0% interest for a limited time (often 12 or 18 months).

- High Approval Rates: The lenders who offer this type of financing specialize in home improvement costs and tend to have more flexible approval criteria.

What to Watch Out For:

- The Post-Promo Rate Increase: If you do not pay off the entire balance before the 0% APR offer ends, the interest rate that takes effect can be very high.

- Limited Shopping: You are using the contractor’s partner lender, so you cannot easily shop around for the best rate from different banks.

No matter which path you take, always read the fine print. A thorough review of the loan agreement is essential before you sign anything. You need to be completely clear on the terms, conditions, and repayment expectations.

Getting Your Ducks in a Row: Prepping for Your Financing Application

Once you have your project quote and a good understanding of the available financing options, it is time to prepare your application. This part can feel intimidating, but a little organization goes a long way toward securing the privacy fence financing you need. Lenders are simply looking for responsible borrowers, and a well-prepared application sends that message.

Think of it as building a strong case for yourself. Lenders want a simple, clear snapshot of your financial health. Having everything ready beforehand makes the entire process smoother for everyone.

Get Your Paperwork Together

Before you begin filling out forms, start by collecting the documents every lender will request. This is not just about being organized; it gives you a chance to spot any potential issues before the lender does.

You will almost always need to provide:

- Proof of Income: Your two most recent pay stubs are usually sufficient. If you are self-employed, plan on needing your last two years of tax returns.

- Identification: A clear copy of a government-issued ID, like your driver’s license, is required.

- Project Quote: This is absolutely essential. A detailed, professional quote from your fence installer (like the free estimate we provide) shows the lender exactly what the funds are for.

- Proof of Residence: A recent utility bill or bank statement showing your name and current address will work.

I recommend creating a dedicated folder—either on your computer or a physical one—for these documents. When a lender requests something, you can send it over in minutes. It shows you are organized and prepared.

Making Your Application Shine

Beyond gathering documents, you can take a few steps to make your application more appealing to lenders. A strong financial profile not only boosts your approval odds but is also your key to unlocking lower interest rates, which can save you a significant amount of money over the life of the loan.

Start with your credit. Your credit score is one of the first things lenders look at, as it provides a quick summary of your borrowing history. A higher score indicates a solid track record of paying your debts on time.

A strong credit score is often required for favorable financing terms. You can learn how to improve your credit score with actionable tips that can boost your approval odds and help you access better rates.

Even small improvements can make a real difference. For example, checking your credit report for errors and correcting any inaccuracies is a simple action that can sometimes give your score a quick boost.

Another metric lenders care about is your debt-to-income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying your existing monthly debts. It helps lenders determine if you can comfortably take on another payment.

For example, if you earn $6,000 a month before taxes and your total monthly debt payments (mortgage, car loan, credit cards) add up to $2,400, your DTI is 40% ($2,400 ÷ $6,000). From a lender's viewpoint, a lower DTI is always better.

Actionable Tips to Boost Your Approval Odds

Before submitting your application, consider these practical steps to present the strongest financial version of yourself.

- Address High-Interest Debt: If you have balances on high-interest credit cards, paying them down can lower your credit utilization and your DTI. This is a powerful two-for-one move that lenders appreciate.

- Avoid New Credit: In the weeks before you apply for fence financing, try not to open any new credit cards or apply for other loans. Every application triggers a "hard inquiry," which can cause a small, temporary dip in your credit score.

- Showcase Stable Income: Stability is a huge plus for lenders. If you have been at your job for a while, that is a great sign. If you recently started a new, higher-paying job, make sure your income documents reflect that increase.

- Partner with a Reputable Contractor: This is an underrated tip. Choosing a well-established and highly-reviewed fence installer can indirectly strengthen your application. Lenders who finance home improvement projects want to see professional, clear quotes. A contractor with a strong reputation, like Connecticut Fence Works, provides the kind of documentation that adds trust and legitimacy to your funding request.

The Easiest Route: Financing Your Fence Through Your Installer

After looking into personal loans and HELOCs, you might be thinking there has to be a simpler way to finance your fence. There is. Many homeowners find that the most straightforward path is financing directly through their fence installer.

Instead of managing communications between a loan officer, a bank, and your fence company, you have one point of contact. This bundles the project and its funding into a single, seamless process. We have built strong relationships with lenders who understand home improvement projects, which almost always results in a smoother, less stressful experience for you.

Why an Integrated Process Just Works Better

The real benefit of handling financing through your installer is simplicity. The people who know every detail of your project are the same ones helping you secure the funds for it. It all starts with one conversation.

When we visit for a free on-site estimate, we do not just talk about post spacing and gate placement. We can discuss your budget and explore financing options at the same time. This helps us understand what you are comfortable with and recommend the best programs from our lending partners.

This all-in-one approach eliminates many of the usual headaches. The advantages are practical and immediate:

- A Simple Application: Forget generic bank forms. These applications are designed for home improvement projects and can often be completed online in minutes.

- Fast Decisions: Because our lending partners know us and our work, they can often provide a decision very quickly—sometimes almost instantly.

- Real Guidance: You are not talking to a random call center. Your fence professional can answer your questions and walk you through the process, offering support you will not find elsewhere.

Getting Access to Better Rates and Promotions

A contractor who offers financing is invested in your approval—it is how the project moves forward. Because of this, our lending partners often provide competitive programs designed for homeowners like you. One of the best deals available is promotional 0% APR financing for a set period, such as 12 or 18 months.

An offer like this allows you to pay for your new fence over time without paying any interest, as long as the balance is paid in full before the promotional period ends. It is an excellent way to manage your cash flow.

Think of it as a great opportunity, but one that comes with a deadline. If the balance isn't paid in time, a high interest rate typically applies to the original purchase amount, starting from the purchase date. Always read the terms carefully.

There is no denying that the demand for residential security and privacy is driving a construction boom. The global fencing market is projected to reach USD 36.84 billion by 2025, with residential projects making up 45.1% of that revenue. Yet, high upfront costs are a major hurdle, deterring up to 40% of potential buyers. Contractor financing bridges this gap, making dream projects possible for families in places like Hartford and Tolland County without the immediate financial burden. You can explore the full fencing market report to see how these financing options are empowering homeowners everywhere.

What to Expect From the Process

When you work with a contractor like Connecticut Fence Works for financing, the journey is transparent and designed to keep your project on track from day one.

It all begins with a free estimate and consultation at your property. We will discuss your goals—whether it is privacy, containing a pet, or securing a pool—and provide a detailed, itemized quote. This is the perfect time to mention you are interested in financing.

From there, we will explain the financing programs our partners offer. We can show you the terms, estimate monthly payments, and highlight any special promotions available. With a clear quote in hand, you can then complete a short application, and our team is there to help if you have any questions.

Once you get approval, you can sign the project agreement, and we will schedule your installation. The lender and contractor handle the payment logistics directly, leaving you to focus on the exciting part—watching your new fence being built.

Ultimately, this approach is built on trust. By choosing one reputable company for both the installation and financing guidance, you get clear communication and total accountability. If you are ready to see how this could work for your project, you can easily request a free estimate from Connecticut Fence Works and discuss your financing needs with an expert.

Common Questions About Privacy Fence Financing

Even after reviewing all the options, you probably still have a few questions. That is completely normal. When considering a major home improvement project, you want to be sure you are making the right financial decision.

Let’s address some of the most common questions we hear from homeowners in Connecticut. Our goal is to clear up any confusion so you can move forward with total confidence.

Can I Finance a Privacy Fence with Bad Credit?

Yes, but it is important to be realistic. Securing financing with a lower credit score is possible, though your options may be more limited and the interest rates will likely be higher. Some lenders specialize in working with borrowers in this situation.

Contractor financing, like the programs our partners offer, can also provide more flexibility than a traditional bank. If your credit is not perfect, here is what we suggest:

- Review your credit report. Know exactly where you stand and check for any errors you can dispute.

- Pay down high-interest debt if possible. Even small reductions in your credit card balances can improve your financial profile.

- Talk to us. An honest conversation about your situation helps us guide you toward the most suitable solutions available.

What Is the Typical Cost for a Privacy Fence in Connecticut?

This is a very common question, and the honest answer is: it varies widely. The final price depends on the total length of the fence, your chosen height, and, most importantly, the material.

To give you a general idea for an average suburban yard, here is a common price range we see:

- Vinyl Privacy Fence: Usually falls between $7,000 and $15,000.

- Custom Cedar or Ornamental Aluminum: As premium materials, these will naturally be at the higher end of the spectrum or even exceed it.

The only way to get a firm number for your financing application is to have a professional visit your property. A free, no-obligation estimate allows us to measure everything, show you materials, and build a detailed quote for your specific project.

How Does Financing My Fence Affect My Mortgage?

This depends entirely on the financing route you choose. If you use a personal loan, a credit card, or contractor financing, it is a completely separate debt. It has no direct connection to your mortgage, and your home is not used as collateral.

However, choosing a Home Equity Line of Credit (HELOC) or a home equity loan is different. With these options, you are borrowing against your home's value. This places a second lien on your property, meaning the new loan is secured by your house. It is a critical distinction to understand before you commit.

Is It Better to Use Contractor Financing or Find My Own Loan?

There are good reasons for both, and the "better" choice really depends on what you value most.

Contractor financing is all about convenience and simplicity. The process is often handled directly through us, your installer. Because we have relationships with lenders, we often see quick approvals and can sometimes offer special promotional rates.

On the other hand, finding your own loan from a bank or credit union gives you the power to shop around. You can compare rates and terms from multiple lenders, which could save you money over the life of the loan.

Our best advice? Get a quote from our financing partner and compare it to one or two pre-approvals you get on your own. This way, you can see all the options on the table and feel confident you are getting the best deal for your new fence.

Ready to transform your property with a beautiful, durable privacy fence? The team at Connecticut Fence Works, LLC is here to walk you through the entire process, from design to financing. Request your free, no-obligation estimate today!